Stay disciplined and don’t despair

Avoiding consensus and crowded positioning is a core contributor to success in generating relatively stable returns.

As central banks continue to withdraw liquidity from the system, this is all the more important. We remain cautious, anticipating a further slowdown in growth as the effects of monetary tightening flow through the system. But there are opportunities, and we will remain disciplined to lean into these as and when they arise.

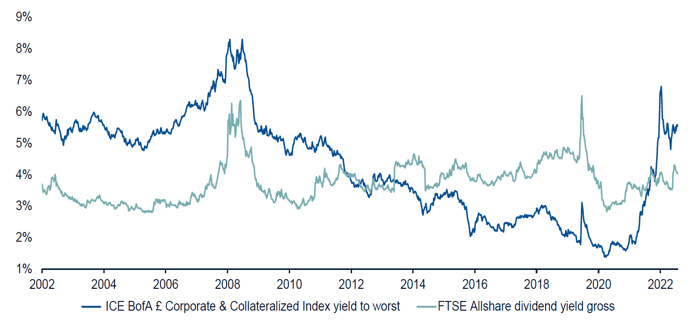

For now, we have a clear preference for government bonds and quality investment grade debt, where yields are above equity earnings yields – something that tends not to last for long.

We also believe the cheap valuations in Emerging Markets (EM) are compelling for long term investors. Having started their tightening cycles sooner, disinflation in EM is widespread and that positions their central banks nicely to start cutting rates, potentially meaningfully, over the year ahead.

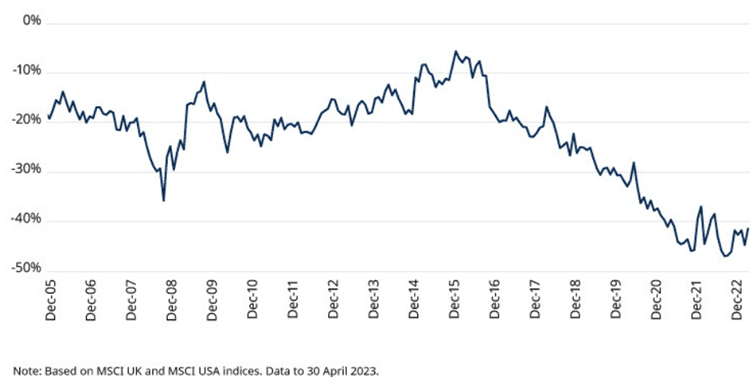

The UK is unquestionably cheap. However, it is also saddled with deep rooted structural challenges. Until a new sustainable investment cycle that drives improved efficiency and productivity emerges, it is likely to remain unloved by global investors. Of course, with expectations so depressed, the potential for upside surprise is all the greater.

…there is cause for some optimism. After the travails of 2022 and the continued monetary squeeze in 2023, our long term capital market assumptions of projected future returns for investors are looking better.

It’s a potholed outlook, so a well-diversified portfolio to protect against recession and persistent inflation is key. The central banks quest to achieve a soft landing looks challenging with increasing risk that something breaks as rates are kept higher for longer. But disinflation is underway and investors will start to look ahead to when interest rates can start to come down.

Attempting to time an inflection point is virtually impossible, and macroeconomic data is expected to be highly variable, so increased volatility is assumed. But there is cause for some optimism. After the travails of 2022 and the continued monetary squeeze in 2023, our long term capital market assumptions of projected future returns for investors are looking better. Sticking to a long term investment plan is a pragmatic and prudent approach to take.

This document is only suitable for financial professionals. Any news and/or views expressed here are intended as general information and shouldn't be seen as a personal recommendation.

An investment’s past performance isn't an indicator of its future performance, and you could get back less than you put in. There's also no guarantee that an investment will meet its objectives.