So where are the opportunities?

Despite the excitement surrounding AI related stocks, especially in the US, investors became increasingly worried in the first half of the year.

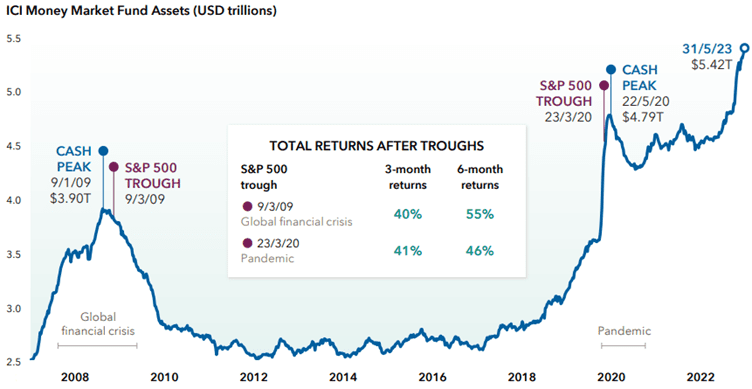

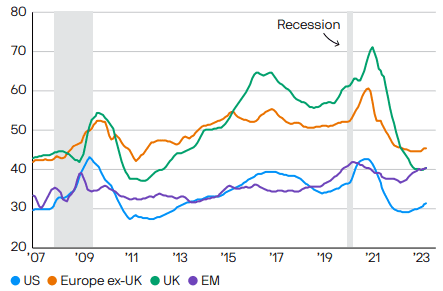

Thanks to attractive nominal short term interest rates, allocations to cash and money market funds are at historic highs.

Investors’ flight to cash has now surpassed that of the pandemic and financial crisis:

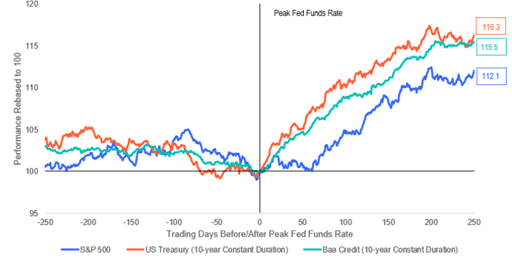

As interest rates peak, the reinvestment risk from short dated bonds increases, with maturing bonds rolling into lower yielding instruments. The prospect of this liquidity being reallocated into longer duration assets over the next 6-12 months is high, most likely into fixed interest where the scope for picking up an attractive yield in conjunction with potential capital gain is not insignificant. History shows that, on average following the peak in interest rates, bonds tend to take a lead over equities.

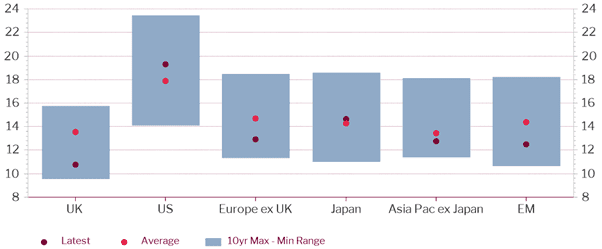

Valuations in equities are not compelling given where we are in the economic cycle. However, consensus earnings expectations are more realistic, following notable downgrades in the first half of the year.

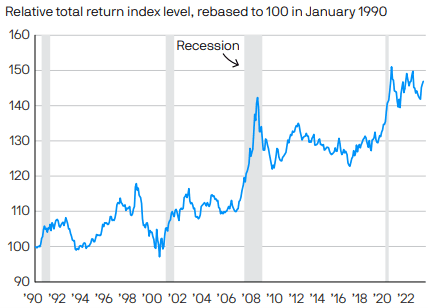

Caution is warranted. Slowing revenue growth combined with margin pressure is likely to limit scope for upside surprise. In this environment, quality, dividends and selectivity are key. Over recent years, quality as a style has been left behind while growth or value has led returns.

During more challenging economic environments however, quality has proven to outperform, offering ballast and resilience to portfolios - something that PIM firmly believe in.

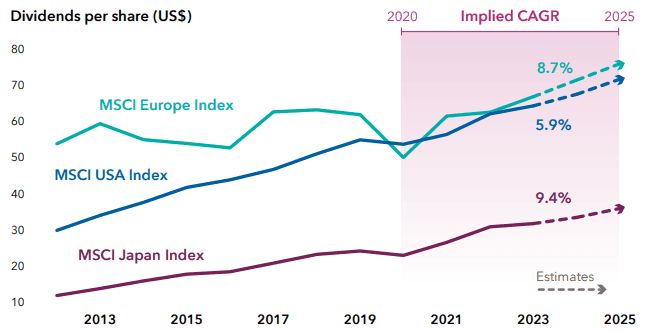

With sluggish growth and higher inflation than we have been used to since the global financial crisis of 2007/8, dividends should be an increasing component of investor total returns in the year ahead. Payout ratios have notably declined since pre Covid, giving scope for resilience in dividend distributions and potential upside surprise.

Dividend growth prospects also appear encouraging as the breadth of sector contribution expands beyond the historic norms. Energy, mining, financials and utilities are joined by cash-rich technology, consumer services and consumer discretionary companies in distributing more to shareholders. With improving dividend growth expected from Japan, US and the EU, geographical diversification is further strengthening the outlook.