What’s in store?

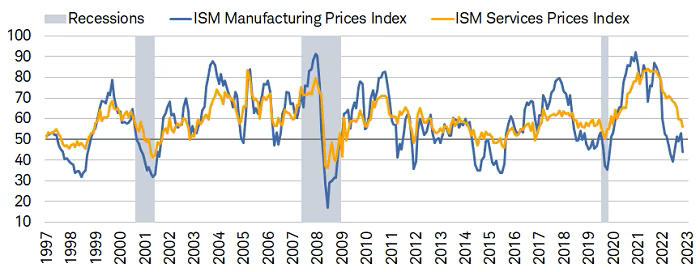

Disinflation is already widespread with the Institute of Supply Management's (ISM) manufacturing prices and services prices indexes both declining.

Energy and commodity prices have contracted significantly and food prices are showing signs of rolling over. Inventories are being proactively sold down as the cost of capital to fund them rises, and the passing of prices to consumers is starting to hit a wall as the cost of living reduces household disposable income.

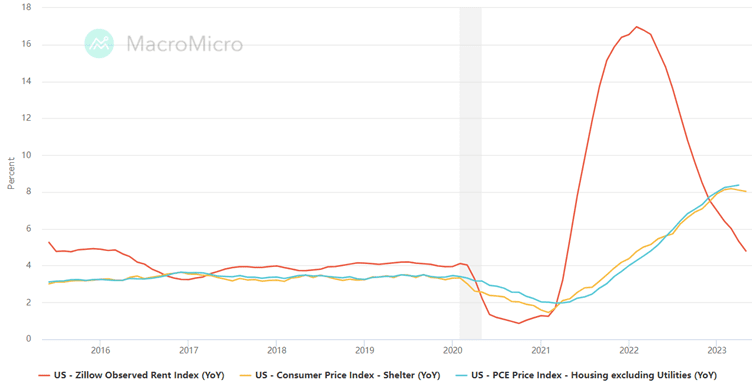

The final sticking point in US inflation is shelter. The measure of owners’ equivalent rent follows the lead of the observed rent index, albeit with a lag. This could see shelter, currently still elevated, almost halve from today’s rate of 8% by the end of the year.

With growth expected to slow as higher interest rates stifle demand, inflation is likely to move closer to central bank targets. The anchoring of long term inflation expectations close to target will help assure central banks, encouraging them to ease up on their monetary tightening crusade.

…the BoE has little option if it’s to re-establish its credibility, so rates can be expected to stay higher for longer.

In the UK, inflation has proved to be broader and more persistent, raising Bank of England (BoE) concerns that it could become entrenched. The source of its persistence is not raising rates more aggressively sooner, labour supply shortages from the wave of early retirees during Covid and loss of European workers post Brexit, plus years of underinvestment constraining competitiveness and productivity.

Higher interest rates may seem like a blunt tool when it comes to addressing these issues. However, the BoE has little option if it’s to re-establish its credibility, so rates can be expected to stay higher for longer. And that points towards a rising probability of recession.

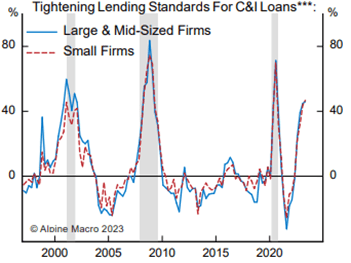

The inevitable credit squeeze that has come from the fastest rate rises for four decades is all too clear in the US Senior Loan Officers Survey, UK Credit Conditions Survey and Bank EU Lending Survey.

All show a marked contraction in credit availability and demand as the cost of credit has taken off.

Credit demand tends to be a reliable lead indicator of economic activity and, when combined with negative growth in money supply, points firmly towards the probability of easing inflation.

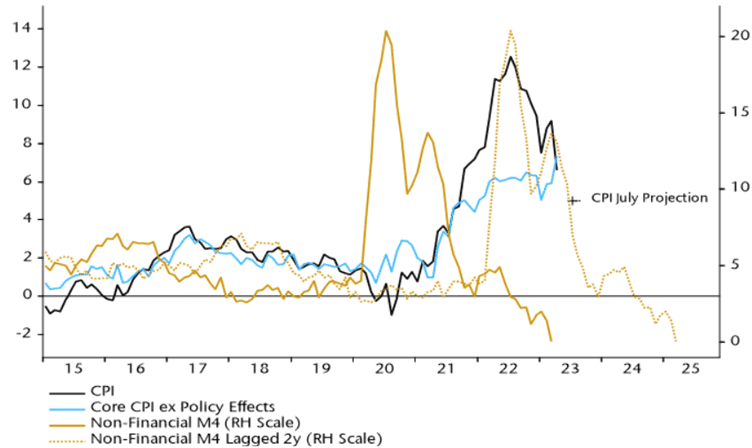

Applying a 2 year lag to the Covid-inspired expansion in money supply aligns neatly with the spike in inflation in 2022. Assuming the same relationship holds in reverse, the contraction in money supply we’re seeing today suggests inflation will wither into 2024, with growth subsequently becoming the primary point of concern.

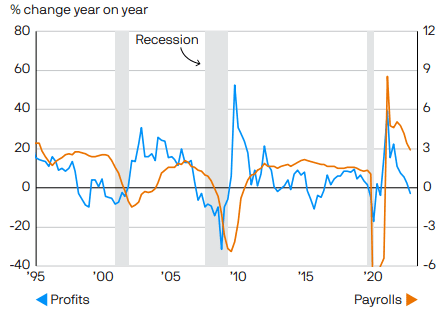

The factor that has managed to defy expectations so far has been the strength of the labour market.

Difficulties in recruiting post Covid mean companies have been reluctant to let people go, even as demand slows. But slowing sales and pressure on margins will, in time, lead to fewer job hires and more layoffs. And cracks are already appearing in the labour market as average hours worked falls, wage increases drop from their highs and overtime shrinks.

US profits and payrolls – weakening profits are normally followed by weakening employment

With inflation at 4% and overnight rates at 5.25% in the US, positive real rates are already in place. The EU and UK are expected to follow as the year unfolds.

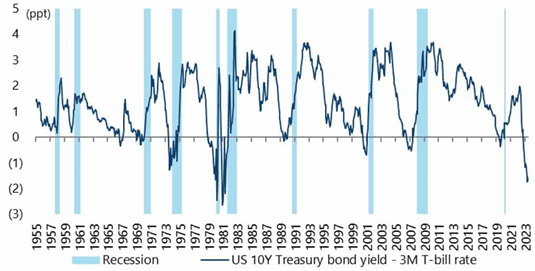

The fixed interest market has been anticipating this for some time, with the yield curve deeply inverted across all maturities. This has been a reliable indicator of recession through recent history, and we have no reason to doubt its predictability this time.

Recession is widely expected, but the question is how deep and long it might be. The consensus answer is short and shallow, with the potential risk of it not occurring at all or that it’s longer than anticipated.

The good news is that current interest rates give central banks scope to cut rates if required. On average in a recession the Fed has cut rates by 450bps, so the prospect of material monetary easing is not insignificant, but only after a notable economic contraction as suggested by lead indicators.

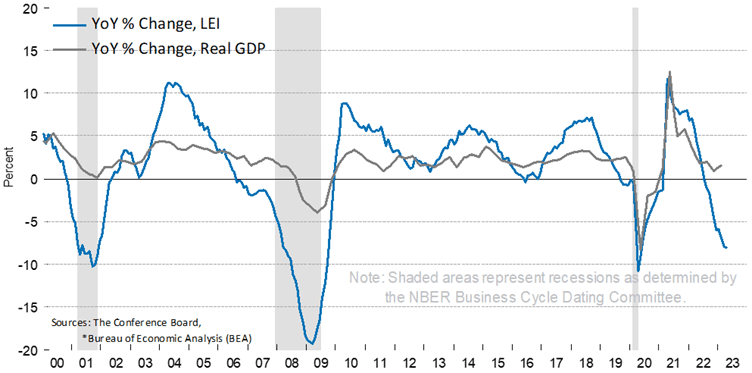

The annual growth rate of the US Lead Economic Index (LEI) continued to decline, signalling weak GDP growth ahead.