2024 Market Outlook

Consensus expectations of recession failed to materialise in 2023, despite persistent monetary tightening by central banks.

The consumer was the mainstay of economic growth and resilience, as labour market strength supported nominal wages. Fiscal expansion, notably in the US, stimulated investment activity which more than offset the slowing effects of higher interest rates. However, it’s uncertain how sustainable these economic drivers will be.

Cumulative savings appear low by historical standards, budget deficits are bloated for this stage of an economic cycle, and the impact of monetary tightening has yet to fully work its way through the system.

This points to a more challenged macroeconomic outlook for 2024, especially when consensus expectations of a ‘soft landing’ are so universal.

The economy is not the market though, so we need to consider broader variables to understand the likely direction of markets including liquidity, valuation and sentiment. Here, there are signs that things may be poised to improve, or at least get less bad. Often in markets less or more is of greater importance than high or low. While exercising care, we are increasingly encouraged by a number of select opportunities for investors that are beginning to emerge. Patience and commitment will be required - it is expected to be a bumpy journey.

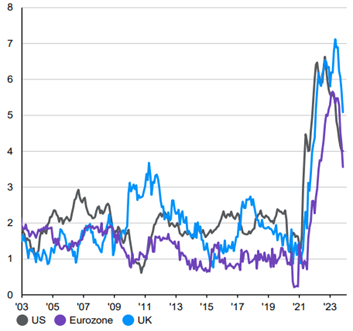

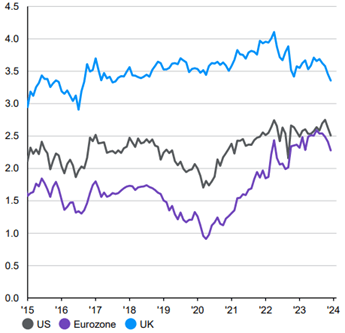

Disinflation is well advanced across most major economies, with interest rates comfortably above GDP growth and higher than core inflation. This restrictive stance by central banks is deliberately designed to slow economic activity and create some slack so that inflation expectations are lowered and price stability targets met.

It would be bold to declare the war against inflation over, but the battle appears to have been won, with long term inflation expectations rolling over. This led the Fed to talk about the timing of rate cuts in its post December meeting press conference, as they shift their focus to limiting risks of recession and supporting growth.

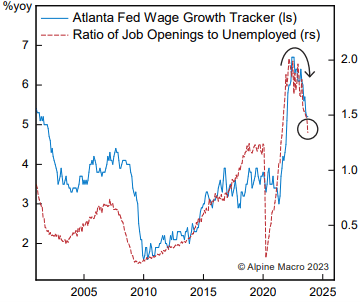

As we move into an election year, it’s not surprising that growth will become the primary point of focus. This is gaining greater attention because strength in the labour market is cooling and the electorates’ focus is shifting from cost of living concerns to worries about job security.

As growth slows, unemployment rises, temporary worker demand falls, quits rates decline, wage pressures ease and job vacancies contract. And this is all before new year corporate budget restraints take effect. These cracks have scope to become chasms, and rather like the path to bankruptcy, can start slowly and unfold rapidly.

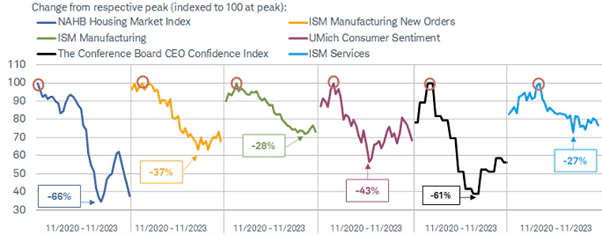

Despite interest rates rising at the fastest pace since the 1980s, economies in 2023 have been far more resilient than we expected. However, the consensus assumption of a soft landing now looks optimistic in our opinion. History has demonstrated that it's notoriously difficult for central banks to achieve, despite their best intentions.

Already in 2023 there have been a number of ‘rolling recessions’ (a term borrowed from Charles Schwab) in housing, manufacturing and even services.

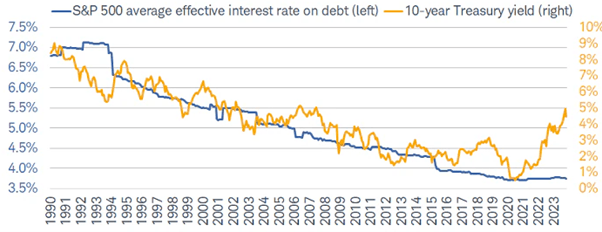

The full effect has yet to be truly felt, because when corporates and household’s current lending terms expire, they’ll need to refinance at much higher rates. For many this means a 50%+ increase on what they're currently paying. This will lead to a squeeze on disposable incomes and corporate growth plans. For example, the average US 30-year fixed rate mortgage has risen from around 3.7% in Q1 2022 to 7.79% at the end of October 2023, while the cost of bank debt for small caps has climbed from around 6.5% to 9.6% over the same period. The subsequent dampening effect on consumption and investment isn't hard to imagine. Combine this with greater incentives to replenish the depleted savings pots used to make ends meet during the cost of living crisis, it’s hard not to conclude the prospect of an imminent slowdown.

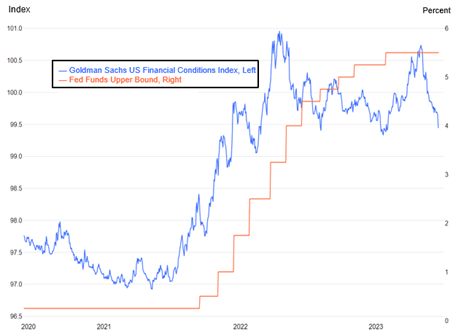

Fortunately, the importance of relativity in investing means that challenge brings opportunity. Markets have begun to discount lower interest rates in anticipation of a weaker near-term outlook. This has led to an easing of financial conditions, which should help to abate some of the financial squeeze.

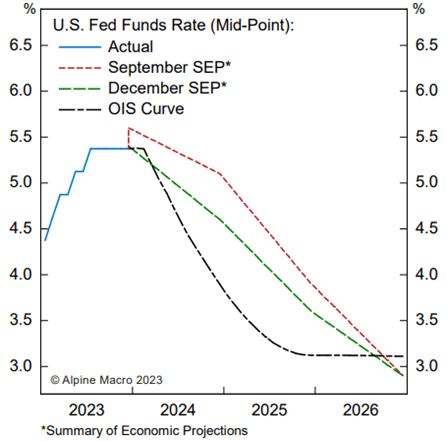

This may be a deliberate ploy by the Fed to get the market to do some of the easing without lowering base rates themselves. However, since the 1960s the Fed has cut rates by an average of 450bps to support and stimulate economic activity. Even if we halve that assumption, the 150bps of rate cuts currently discounted in the market for 2024 has scope for further positive surprise if a slowdown becomes a recession. Replacing the ‘higher for longer’ with ‘lower and faster’ is something markets will keenly embrace.

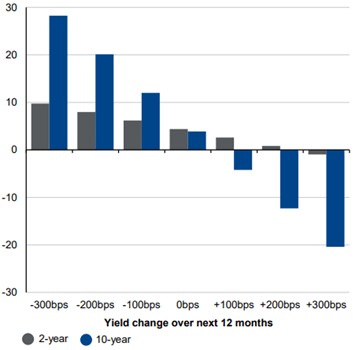

This bodes well for fixed interest, where yields are meaningfully more attractive than the depressed levels post pandemic and the Global Financial Crisis. They also offer scope for capital protection and appreciation if interest rates come off as we expect they will.

Furthermore, we believe negative correlations between fixed interest and equities will begin to reassert themselves as slower growth forces equity analysts to downgrade their earnings forecasts.

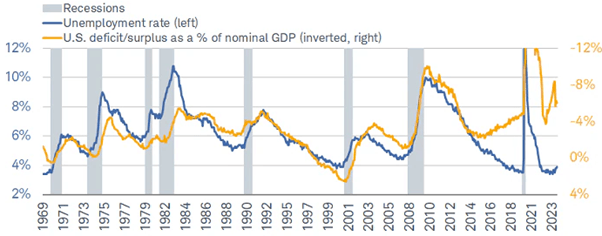

Debt and its sustainability is one area that does look challenging. With Debt:GDP ratios commonly around or in excess of 100%, there are growing concerns about the ability to service that debt. The US budget deficit expanded to $1.7trillion in fiscal year 2023, representing 6.3% of GDP. This is at a time when the unemployment rate was close to a record low. If a slowdown leads to a rise in unemployment, pressure on the fiscal deficit will grow. This is a worry that we will continue to monitor, but we expect the market will continue to function effectively, albeit with a higher term premium to compensate investors for the additional risk.

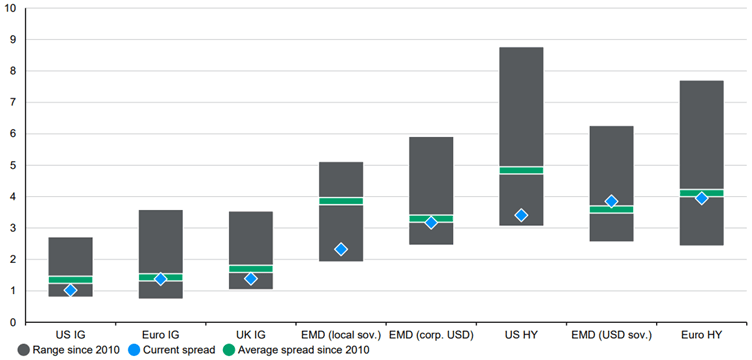

On a risk adjusted returns basis, fixed interest looks relatively more attractive than equities at this stage of the cycle. Within fixed interest, government bonds (rates) look more appealing than corporate bonds (credit), where spreads have narrowed to below historical averages. However, because of the way they’re constructed, passive credit indices hide a range of attractive opportunities for active managers in quality issuers. The key is selectivity.

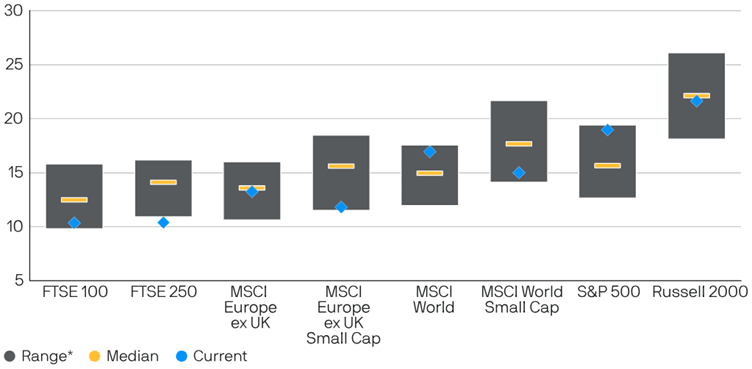

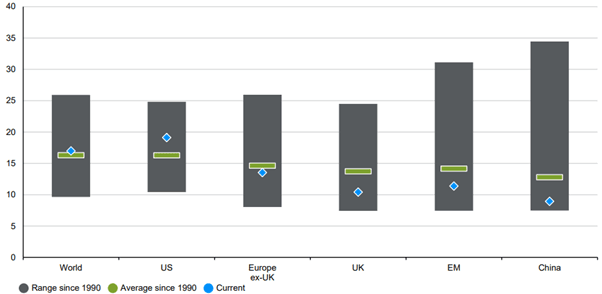

For global equities, valuations look unexciting, sitting just above historical averages, primarily driven by mega caps in the US. Earnings forecasts look vulnerable to downward revision, though there are a few long-term opportunities that do look increasingly interesting.

Mid and small caps look attractive versus core indices and against their own history. Having been aggressively sold off through 2023, ownership is light and expectations low. Having already survived their own recession as credit conditions tightened, those remaining can be seen as survivors, something that’s not reflected in their PE multiples.

Emerging market central banks have been ahead of their developed market peers. So we believe they're well placed to rally as they cut rates ahead of the Fed.

Emerging Markets (EM) also represent good long term investment opportunities. In the past, rate hikes like those in 2022/23 would've led to increased EM currency volatility and probable recession. This hasn't been the case this time, because EM central banks have been ahead of their DM peers. So we believe they're well placed to rally as they cut rates ahead of the Fed. Their fiscal policy targets support for domestically oriented growth, and their perceived sensitivity and dependence on international trade is lessening, though the recovery of global manufacturing post the 2023 slump is expected to be tentative.

Alternatives are another asset class that have had a challenging 2023, such as infrastructure, property and commodities. As we pass peak interest rates, we believe the natural inflation protection characteristics of these sub asset classes will be sought after. As advocates of diversification and given the uncertain outlook, we also like uncorrelated strategies through hedge funds and absolute return. Both support the consistency of delivery of attractive risk adjusted returns through the economic cycle.

Finally, quality is a style that has frustratingly fallen between the cracks of growth and value in 2023. We believe that, as economic momentum slows, investor focus will return to seeking quality companies with a proven capability to deliver compounded returns. The consistency and stability of revenue growth, profitability and cashflow is expected to be of growing importance for investors, commanding a higher multiple, and supporting attractive returns.